Did you know that in 2026, many Georgia insurance carriers are shifting older roofs to Actual Cash Value policies, which could leave you responsible for thousands of dollars in depreciation costs? Learning how to file a roof insurance claim in Georgia correctly is no longer just about fixing a leak; it's about protecting your home's equity against shifting industry standards. You've likely felt the stress of a sudden storm and the immediate dread of dealing with confusing jargon or the fear that your premiums will skyrocket if you speak up.

At Supreme Roofing and Reconstruction, we believe you shouldn't have to face adjusters alone or settle for less than you deserve. We promise to help you manage this process with confidence using our expert-led restoration framework. This guide provides a clear, step-by-step path to securing full replacement coverage while ensuring you stay compliant with Georgia laws like House Bill 423. We'll walk through the critical 15 day response timelines, the importance of professional documentation, and how to achieve a meticulous, stress-free restoration for your family home.

Key Takeaways

- Understand the specific criteria for "un-repairable" storm damage under Georgia law to determine if your roof qualifies for a full insurance replacement.

- Learn the professional sequence of how to file a roof insurance claim in Georgia, starting with a meticulous inspection before you alert your insurance carrier.

- Decode the financial difference between Replacement Cost Value (RCV) and Actual Cash Value (ACV) policies to accurately predict your out-of-pocket restoration costs.

- Discover how the insurance supplement process identifies hidden damage to critical components like flashing and starter shingles that adjusters frequently overlook.

- Benefit from a stress-free restoration by partnering with a local expert who manages the technical documentation and ensures your home meets Supreme quality standards.

Navigating Roof Insurance Claims in Georgia’s Storm Climate

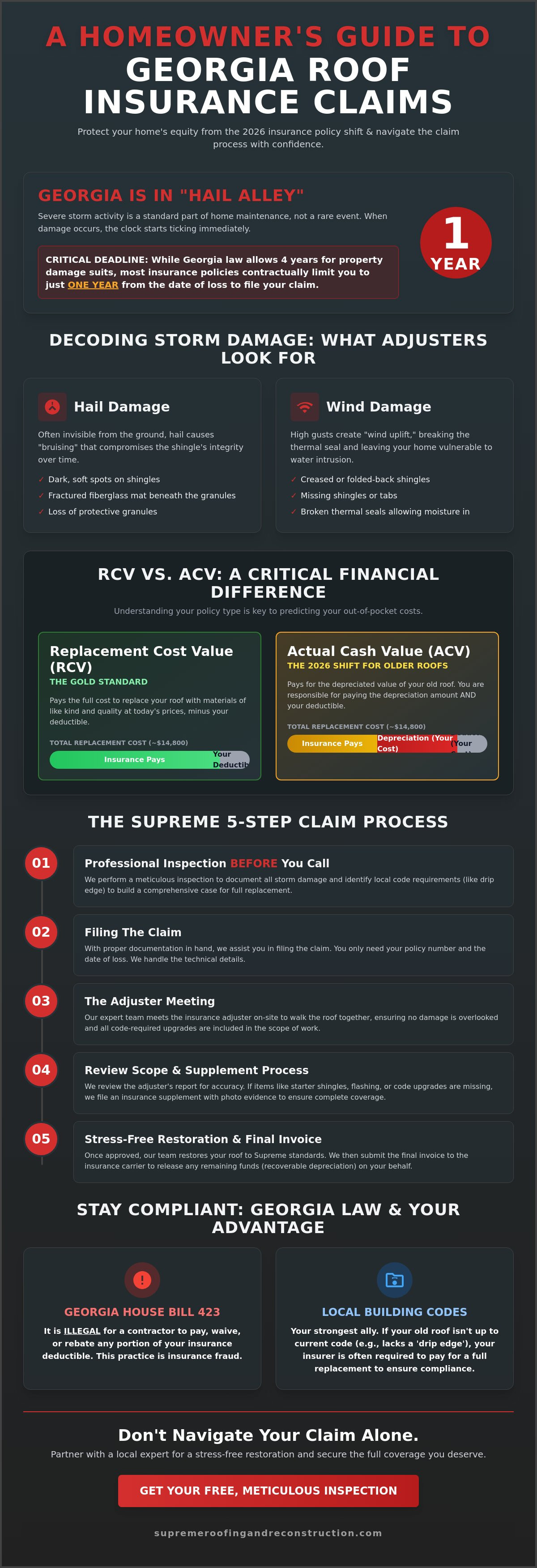

Georgia homeowners live in what industry experts often call "Hail Alley." This region experiences some of the most consistent and severe storm activity in the Southeast, making storm damage a standard part of home maintenance rather than a rare occurrence. Understanding how to file a roof insurance claim in Georgia starts with recognizing that your roof is a complex system designed to withstand these elements, but even the highest quality shingles have a breaking point. When a storm strikes, the damage isn't always obvious from the driveway, yet the clock starts ticking the moment the clouds clear.

Under Georgia law, a roof is often deemed "un-repairable" if the existing shingles have become too brittle to withstand a standard manipulation test. This means if a contractor cannot lift a shingle to replace a damaged neighbor without causing it to crack or lose its seal, a full replacement is required to maintain the home’s integrity. We define storm restoration as a comprehensive return to pre-storm condition, ensuring every component from the decking to the ridge vents meets Supreme standards of safety. While Georgia's general statute of limitations for property damage is four years, your specific homeowners insurance policy likely contractually shortens this window to just one year from the date of the loss. Delaying your inspection can jeopardize your ability to secure the coverage you've paid for through years of premiums.

Wind vs. Hail Damage: What Georgia Adjusters Look For

Hail damage in Georgia rarely looks like a gaping hole. Instead, it manifests as "bruising," where the impact of a hailstone fractures the fiberglass mat beneath the granules. These dark, soft spots are the first signs of failing shingle integrity. Wind damage is equally deceptive. High gusts create "wind uplift," which breaks the thermal seal and creates "creased shingles." These creases are often invisible from the ground, but they allow Georgia’s high humidity to seep into the sub-structure. This moisture leads to rapid wood rot and mold growth, compromising your home's value and your family's health.

The Role of Local Building Codes in Your Claim

Local building codes are your strongest ally during a claim. Georgia code now requires the installation of a "drip edge" on all eaves and rakes to prevent water from wicking into the fascia. If your current roof lacks this feature, insurance carriers are often legally required to pay for a full replacement to bring the structure up to current legal standards. This is where "Code Upgrade" or Law and Ordinance coverage becomes vital. At Supreme Roofing, we use specific codes from Cumming, Atlanta, and surrounding municipalities to justify full coverage. We ensure your new roof is not just a patch job, but a legally compliant, superior shield for your property.

Deciding to File: Deductibles, RCV, and Policy Math

Filing a claim is a significant financial decision that requires more than just spotting a few missing shingles. Before you initiate the process, you must run the "deductible math" to ensure the claim works in your favor. With the average full roof replacement in Georgia costing approximately $14,800 as of 2026, most homeowners find that a storm-related claim provides a massive return on their policy investment. However, if your damage is minor and the repair cost falls below your $1,000 or $2,500 deductible, filing could negatively impact your claim history without providing any immediate payout. Understanding these numbers is the first step in learning how to file a roof insurance claim in Georgia successfully.

You should also be wary of any contractor who offers to "cover" or "waive" your deductible. Under Georgia House Bill 423, it's strictly illegal for a roofing contractor to pay or rebate any portion of a homeowner's insurance deductible. This practice constitutes insurance fraud. We prioritize transparency and integrity, ensuring you stay compliant with state law while maximizing the legitimate benefits of your policy. If you feel your carrier is unfairly withholding funds or acting in bad faith, you can file a complaint with the Georgia Department of Insurance to protect your rights.

RCV vs. ACV: A Critical Comparison

The type of policy you hold dictates your out-of-pocket costs. A Replacement Cost Value (RCV) policy is the gold standard; it pays the full cost to replace your roof today, minus your deductible. In contrast, many 2026 policies are shifting toward Actual Cash Value (ACV) for roofs older than 15 years. ACV only pays for the depreciated value of the shingles, which often leaves seniors and families with a massive financial gap. If you're unsure which policy you have, our team can help you review your summary of coverage to identify potential risks.

| Expense Category | RCV Policy (Full Replacement) | ACV Policy (Depreciated Value) |

|---|---|---|

| Total Replacement Cost | $20,000 | $20,000 |

| Homeowner Deductible | $1,000 | $1,000 |

| Depreciation (15-year-old roof) | $0 (Recoverable) | $10,000 (Non-recoverable) |

| Total Out-of-Pocket | $1,000 | $11,000 |

Premium Hikes and 'Acts of God'

A common fear is that filing a claim will cause premiums to skyrocket. In Georgia, insurance companies generally cannot raise your individual rates solely because you filed a single "Act of God" claim, such as hail or wind damage. These are considered no-fault events. However, if an entire zip code is hit by a catastrophic storm, the carrier may raise rates for the whole area to balance their risk. This means your rates might go up even if you don't file, so it makes sense to utilize the coverage you're already paying for. Leaving storm damage unaddressed actually poses a higher risk; carriers may issue a non-renewal notice if they discover an aging, damaged roof during a routine inspection.

The 5-Step Georgia Roof Insurance Claim Process

Success in the insurance world relies on order and evidence. Learning how to file a roof insurance claim in Georgia isn't just about making a phone call; it's about building a case for your home's restoration. We've streamlined this complex journey into a transparent, five-step framework designed to eliminate stress and maximize your coverage. By following this sequence, you ensure that every technical detail is captured before the insurance company’s mandatory 15-day response window begins.

- Step 1: The Professional Inspection: We identify microscopic damage that adjusters often miss during a quick walk-around.

- Step 2: Filing the Claim: You contact your carrier with our documented evidence in hand to secure your claim number.

- Step 3: The Adjuster Meeting: We meet the insurance representative on your roof to ensure they see every bruised shingle and creased edge.

- Step 4: The Supplementing Phase: We negotiate for missing items like drip edge or flashing that the initial estimate may have excluded.

- Step 5: Production and Depreciation Recovery: We install your new roof and submit final paperwork to release your remaining policy funds.

The Critical First Inspection

Calling a contractor before you call your agent is the safest way to protect your claim history. If you file a claim and a contractor later finds no damage, that "zero-pay" claim still stays on your record. At Supreme Roofing, we use high-resolution imagery and 10x10 "test squares" to provide an honest, data-driven assessment. We also look for "collateral damage" to items like gutters and siding. Documenting these secondary impacts strengthens your case by proving the storm's intensity was high enough to compromise your roof's shingle integrity.

Winning the Adjuster Meeting

The adjuster meeting is the most pivotal moment in the process. Having a local storm damage restoration expert present ensures the adjuster sees the same damage we do. We act as your "Expert Protector," using Xactimate, the same estimating software used by carriers, to speak their language fluently. If an adjuster suggests a "partial approval" or a simple repair, we use our physical evidence and knowledge of Georgia building codes to justify a full replacement. This proactive approach prevents the common "denial and appeal" cycle that frustrates so many homeowners.

Handling Denials and the Power of Supplements

Receiving a denial letter from your insurance carrier can feel like a door slamming shut on your home's safety. In Georgia's complex insurance market, a denial is rarely the final verdict; it's often just the first step in a professional negotiation. Industry data indicates that approximately 70% of initial insurance estimates are underfunded, missing critical components required for a code-compliant installation. If you are learning how to file a roof insurance claim in Georgia, you must understand that the first "no" is frequently a request for more evidence. We act as your steady hand in this crisis, providing the technical documentation needed to turn a rejection into a full approval.

Common Reasons for Claim Denials in Georgia

Adjusters frequently cite "wear and tear" or "mechanical breakdown" to avoid paying for storm-related losses. They may claim your shingles are simply reaching the end of their life cycle rather than acknowledging the bruising from a recent hail event. If your roof was installed poorly by a previous contractor, an adjuster might use "improper installation" as grounds for denial. We counter these arguments by focusing on "repair-ability." If the shingle integrity is so compromised that a simple repair is impossible without damaging surrounding areas, Georgia law often necessitates a full replacement. Even if you've missed the standard one-year filing window, certain policy endorsements or documented "latent damage" can provide a path for a successful appeal.

The Supplementing Strategy

The "Supplement" is our most powerful tool for ensuring your home is restored correctly. A supplement is a line-item request sent to the adjuster for materials or labor costs that were omitted from the original estimate. We use Xactimate, the industry-standard pricing software, to ensure our costs align perfectly with what the insurance company expects to pay. This process is vital because many adjusters miss "hidden" items like rotted decking, precision flashing, or starter shingles that only become visible during the tear-off phase.

Our meticulous approach ensures you receive a Supreme-standard roof replacement without unexpected out-of-pocket expenses. If an adjuster remains stubborn, we can request a "Ladder Assist" or a second inspection with a field supervisor to review our high-resolution evidence together. We don't just accept the first check; we fight for the full amount required to rebuild your home with unmatched quality. If you've recently received a denial or an underfunded estimate, contact our team for a secondary review of your claim documents today.

The Supreme Approach: Stress-Free Restoration in Georgia

Understanding how to file a roof insurance claim in Georgia is only half the battle; the other half is ensuring the actual restoration meets the highest standards of craftsmanship and durability. At Supreme Roofing and Reconstruction, we act as your Expert Protector from the initial damage assessment to the final shingle installation. We recognize that property damage is a major life stressor, which is why our process is designed to be entirely hands-off for the homeowner. While you focus on choosing the perfect shingle colors to enhance your curb appeal, our team manages the complex technical documentation and direct communication with your insurance carrier.

Our commitment to excellence starts with the materials we select. We utilize only high-quality, impact-resistant shingles that are specifically engineered to withstand the 2026 Georgia storm climate. These materials provide a superior shield against the bruising and granule loss discussed in previous sections, often leading to lower future premiums for homeowners. Because we are rooted in Cumming, Atlanta, and Marietta, our local accountability is unmatched. We don't just finish a job and disappear; we provide a sturdy, long-term warranty backed by a neighborly commitment to our community. This local presence is vital because it ensures that your roof is installed according to the specific regional codes that justify your full insurance coverage.

Beyond the Roof: Gutters, Siding, and Painting

Storms rarely limit their damage to just your shingles. High winds and hail often compromise your home’s entire exterior envelope, affecting gutters, siding, and trim. We streamline your entire restoration by serving as your single point of contact for all exterior needs. This integrated approach ensures perfect color matching across every element of your home, preventing the mismatched look that often occurs when using multiple contractors. Whether you need a full siding replacement or professional exterior painting services to refresh your home’s appearance, we ensure the final result is seamless and adds maximum value to your property.

Ready to Restore Your Home?

Timing is everything when it comes to property protection. With Georgia's storm seasons becoming increasingly unpredictable, leaving a compromised roof exposed to the elements is a risk you don't have to take. Most insurance policies require you to act within one year of the date of loss, and waiting too long can lead to denied claims or secondary issues like internal wood rot. We invite you to schedule a complimentary Supreme Inspection today to get an honest, expert assessment of your home's condition. Let us handle the heavy lifting so you can enjoy the peace of mind that comes with a meticulously restored home.

Schedule your stress-free storm damage inspection with Supreme Roofing and take the first step toward a permanent, high-quality solution for your home.

Secure Your Home’s Future with Confidence

Your home is your most significant investment, and navigating the aftermath of a Georgia storm shouldn't be a source of anxiety. We've explored the critical differences between RCV and ACV policies and the strategic importance of the supplementing phase. By understanding how to file a roof insurance claim in Georgia with the right evidence, you move from feeling overwhelmed to having total control over your restoration. Success isn't just about getting a check; it's about ensuring every shingle and flashing detail meets the highest standards of shingle integrity.

Supreme Roofing and Reconstruction has been a steady hand for homeowners since 2016. With thousands of Georgia roofs restored and deep expertise in Xactimate estimating, our local Cumming-based team provides the authoritative advocacy you need across the entire Atlanta metro area. We don't just build roofs; we protect families with meticulous craftsmanship and transparent communication. Don't let confusing paperwork or difficult adjusters stand in the way of your home’s safety. Get Your Professional Storm Damage Assessment from Supreme Roofing today. We’re ready to be your local ally and guide you through a seamless, stress-free restoration process.

Frequently Asked Questions

Will my insurance rates go up if I file a roof claim in Georgia?

Your individual insurance rates typically won't increase solely because you file a single weather-related claim in Georgia. These are legally classified as no-fault events or "Acts of God." However, if a major storm impacts your entire zip code, the insurance company might raise premiums for the whole area to adjust for increased risk. It's often better to utilize the coverage you've already paid for rather than leaving damage unaddressed.

How much damage is needed to justify a full roof replacement claim?

A full replacement is usually justified when the storm damage is so extensive that a repair is technically impossible. In Georgia, adjusters look for a specific number of hail strikes or wind-damaged shingles within a 10-foot by 10-foot "test square." If the shingles are too brittle to lift and replace without cracking, the entire slope or roof must be replaced to maintain its structural integrity and meet local building codes.

What happens if the insurance company's estimate is lower than the contractor's?

When an insurance estimate comes in lower than a contractor's, we initiate the supplementing process to bridge the gap. We use industry-standard Xactimate software to provide the adjuster with photographic evidence of missing line items like drip edge or flashing. This collaborative approach ensures the insurance company pays the actual market rate for materials and labor. It's a standard part of how to file a roof insurance claim in Georgia successfully.

Can I use the insurance money for something other than the roof?

You shouldn't use insurance claim funds for other home projects because most policies require proof that the specific repairs were completed. If you have a Replacement Cost Value policy, the insurance company will only release the final depreciation check after receiving a completion certificate and invoice. Using the money for other purposes could be considered insurance fraud and may leave you without a valid warranty or future coverage.

How long does the roof insurance claim process take in Georgia?

The typical roof claim process in Georgia takes between 30 and 60 days from the initial inspection to the final shingle installation. Georgia law requires insurance carriers to acknowledge your claim within 15 days of filing. Once the adjuster meeting occurs and the estimate is approved, the actual roof replacement usually takes only one or two days. Understanding how to file a roof insurance claim in Georgia includes planning for these administrative timelines.

What is a 'deductible' and do I have to pay it upfront?

A deductible is your contractually agreed-upon portion of the repair cost, and you'll pay it directly to your contractor rather than the insurance company. Under Georgia House Bill 423, it is illegal for a contractor to waive or "eat" your deductible. You'll typically pay this amount when the materials are delivered or once the job is complete, depending on your specific agreement with a professional restoration partner like Supreme Roofing.

Does insurance cover roof leaks that happened before the storm?

Standard homeowners insurance policies don't cover pre-existing leaks or damage caused by a lack of maintenance. Insurance is designed to address sudden and accidental losses like those from a specific wind or hail event. However, a major storm can often worsen minor existing issues. We perform a meticulous inspection to distinguish between long-term wear and new storm damage to ensure your claim is accurate, honest, and stands up to scrutiny.

What if my insurance company only approves a partial repair instead of a full replacement?

If your insurance only approves a partial repair, we can challenge the decision using a repairability test. This involves demonstrating that the surrounding shingles are too brittle to withstand the manipulation required for a patch. Additionally, if the existing shingles are discontinued and a reasonable color match isn't available, we can often leverage Georgia’s matching standards to justify a full replacement of the entire slope or roof to maintain your home's value.